Wealth Management Services

We offer a complimentary portfolio review and proposal for prospective clients. Please contact us for more information, or click on our links to peruse our introductory information.

Through our Professional Asset Management (PAM) service, we work with clients to define their financial goals, and then adopt and implement concrete steps to achieve those goals.

We manage taxable accounts, IRAs, pension plans, trusts, and other account types individually or on a combined basis. PAM is designed for clients with investable assets of $300,000 or more, but we encourage anyone with financial planning or investment management questions to contact us regardless of their level of wealth.

When you work with AIS, you will work with a team that includes:

Financial Planner

A Financial Planner will look at the “big picture” financial situation and help establish an initial asset allocation plan consistent with your goals.

Investment Advisor

An Investment Advisor, the quarterback of your AIS team, will implement the agreed-upon portfolio and manage your investments on an ongoing basis.

Client Services Associate

Helps establish accounts with the custodian and is available for any questions that arise. The CSA also prepares your quarterly AIS financial reports.

Our process is as follows:

- Establish clear and attainable financial goals, including but not limited to retirement planning, saving for college, debt management, tax planning, legacy planning, and charitable giving.

- Gather all relevant financial data, including income, expenses, assets, and liabilities as well as expectations for the future.

- Analyze the data, develop a financial plan, and portfolio recommendation.

- Finalize a strategic asset allocation plan tailored to your goals and risk tolerance. We can coordinate the portfolio allocation across all client holdings to incorporate those not managed by AIS.

- Implement the agreed-upon recommendations as efficiently as possible, with taxes as a primary consideration. AIS will assist you in establishing accounts with a qualified, independent third-party custodian of your choosing (e.g., Charles Schwab Institutional or TD Ameritrade Institutional) where we will have discretionary investment authority to manage assets on your behalf.

- Monitor. AIS stands ready at all times to implement changes to your investment accounts as necessary. We will keep the portfolio allocation within a target range by re-balancing when cost-effective. Adjustments to the plan will be made as necessary. In taxable accounts we seek to optimize after-tax returns through tax-loss harvesting.

- Communicate. You will receive statements and trade confirms directly from your custodian and quarterly reports from AIS. We are always available to discuss progress toward your financial goals and assist with any financial questions that arise.

AIS Investment Strategy

Markets Work: Don’t Overpay for Returns

Market prices reflect the consensus estimate of millions of market participants – professional traders, retail investors, pension funds, high-frequency traders, speculators, and everything in between. Although it is alluring to believe that we can “beat the market,” academic and empirical research shows there is no effective means of consistently identifying “bargain priced” securities or predicting future prices. In other words, “markets work.”

Rather than try to “beat the market” or “time the market” we identify asset classes, which provide robust historical returns that are not strongly correlated with one another. We then select from these classes to design a portfolio tailored to each client’s situation and tolerance for risk.

Too many investors are sold a strategy that promises to beat the market, only to find themselves consistently lagging, especially after accounting for fees. We strongly believe that any cost that comes between an investor and the returns of the market are an explicit hurdle that must be minimized.

Diversification

There is no such thing as a “free lunch” in investing as risk and reward are related. However, comprehensive portfolio diversification can mitigate many risks.

The idea of diversification is that when one asset class is losing value, often another is gaining, or at least losing less. For instance, during the financial crisis in 2008, many of our clients held high-quality bonds and gold which helped offset the poor performance of stocks. Through prudent diversification, we believe that we can maximize return for a given level of risk

We identify index-type mutual funds and ETFs that allow us to optimize the risk-return trade-off:

- We invest across the entire U.S. stock market to “diversify away” both company-specific and industry-specific risk, neither of which provide higher expected returns as compensation.

- We provide exposure to international stocks in order to similarly “diversify away” country-specific risk.

- To offset the volatility in these global stock markets, we utilize cash, gold, fixed income and global real estate (REITs).

Discipline

A primary function as your investment adviser is to provide the discipline to stay the course. Inevitably, portfolios values are going to fluctuate between good times and bad. The worst thing an investor can do is to behave the way our primal brains have taught us – that is, to run away when markets are falling. As your investment adviser, we aim to prevent this tendency in two ways:

- We assess your risk tolerance in advance and structure your portfolio accordingly.

- During periods of duress, we help you re-focus on your long-term financial goals instead of short-term market fluctuations. We urge you to call us to discuss market fluctuations, the economy, and anything else that is on your mind, so that we can help you cope with the anxiety. We take pride in our composure and discipline in the face of turmoil.

Stock Portfolio “Tilts”

For clients willing to embrace greater risk, we can “tilt” toward factors that have historically provided additional return to compensate the higher risk assumed.

Academics have identified several prominent “factors” that help explain equity (stock) returns. We focus on two of these factors that can be readily captured and implemented within a portfolio without adding significant costs: size and value. These return factors appear repeatedly across time spans and in different countries, meaning we are confident in their long-term ability to provide higher expected returns.

Factor “tilts” can be achieved by using mutual funds provided by our primary fund provider, Dimensional Fund Advisors, which places greater weight on these factors in their mutual funds. The appropriate amount of “tilt” depends on each client’s ability to withstand market volatility and to accept returns that deviate from major market indices such as the Dow Jones Industrial Average or S&P 500.

Bond Portfolio “Vectors of Return”

Bonds serve as a source of stability to counter the volatility of stocks. Generally, we restrict our fixed income holdings to government securities and investment-grade bonds, which have low risk of default, and bonds with short-term maturities, which are not highly sensitive to interest-rate changes.

For investors willing to take on incrementally more risk in the bond portion of their portfolios, we will consider using longer duration and/or “extended quality” issues. For investors that are more sensitive to inflation risk, we also incorporate Treasury Inflation-Protected Securities (“TIPS”). The primary bond funds we use maintain average maturities that range from less than 3 years to more than 6 years and range in average credit rating from BBB to AA.

Gold

We often employ gold in portfolios for investors who are sensitive to the potential for major market disruption or extreme price inflation. Many of our clients have found that owning gold can be a source of comfort during periods of financial distress. Gold appreciated sharply during the darkest moments of the market meltdown of 2008. This helped some investors avoid the fate of others who panicked and sold their stocks near the stock market bottom.

Overview of Fees

Fees are a critical metric when evaluating any investment adviser.

AIS Advisory Fees

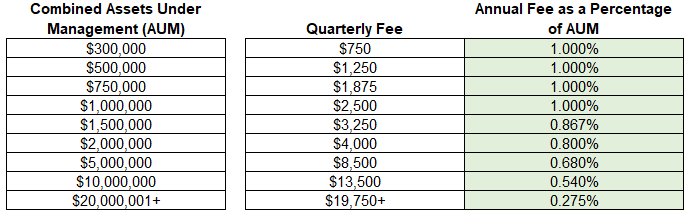

The fees received by AIS are calculated based on the combined values of all managed accounts. An example of our current fee schedule is provided below. Our comprehensive asset management service is called Professional Asset Management (PAM) and example fees can be seen below. Our complete standard fee schedule is provided in AIS’s Disclosure Document.

Fee Calculator

AIS’ standard fee schedule is provided for informational purposes only and is subject to change. AIS retains the right, in its sole discretion, to negotiate alternative fees with its investment advisory clients on a client-by-client basis. In negotiating alternative fees, AIS considers the circumstances and needs of the particular client, including such factors as complexities in the client’s financial situation, nature of the assets to be placed under AIS’ management and/or supervision, whether AIS is engaged to manage and/or supervise related accounts, and potential for future placement of additional investment assets under AIS’ management and/or supervision.

Accounts also incur other fees and expenses, including but not limited to brokerage commissions, mark-ups and mark-downs, dealer spreads or other costs associated with the purchase and sale of securities and other investments, custodian fees, interest and taxes, for payment of which Client is solely responsible.

Mutual Fund Expenses

We primarily use mutual funds and ETFs for most client portfolios. AIS receives no compensation from any fund provider, either directly or indirectly. We have no incentive to offer funds with “sales loads” or 12b-1 fees; in fact, we actively seek to avoid such funds. We typically use funds that range in cost from 0.05% to 0.60%. Most clients incur average fund expenses of about 0.30%. Clients should refer to the particular fund’s prospectus for specific fees and other charges imposed by the fund.

Transaction Fees

We have no incentive to trade other than to keep your holdings in line with our recommendations and any reasonable client-imposed restrictions. Aside from the initial transactions necessary to establish your AIS portfolio(s), trading is typically limited to occasional rebalancing which should therefore have a relatively limited impact on total returns. Charles Schwab and TD Ameritrade provide the following trade commission schedules for households meeting certain account requirements*.

Frequently Asked Questions

Q: Is now a good time to invest?

A: Yes. As the adage goes: “The best time to invest was 20 years ago; the second best time is now.” It is impossible to predict the direction of markets in the short-term. If you have long-term financial goals, it is wise to invest in order to make progress toward those goals. We urge our clients not to get caught up in short-term momentum or what has happened recently, and focus on the long-term future.

Q: What do you expect for stock and bond returns?

A: We do not produce any forecasts regarding the direction of markets. Historically, over long periods of time such as 15-20 years, stocks tend to outperform bonds, but with greater volatility. Likewise, small cap and value stocks have tended to outperform the broad stock market over long periods with more volatility.

Q: How have your returns been?

A: It depends on the investor. Returns are the result of how much risk you are willing to take. Those who have taken on more risk – a higher allocation to stocks – generally have higher long-term returns than those who take on less risk. Those higher returns come with more volatility. For example, during the financial crisis, risky investors had to endure lower troughs than those who held a more balanced portfolio (i.e., a higher allocation to bonds, cash, and gold).

Every investor has unique circumstances, and therefore every investor has a unique portfolio. Market returns have been quite favorable over the last several years, and the investments we use have effectively captured these positive market conditions at a low cost.

Q: How much do you charge?

A: We charge an advisory fee that is calculated based on the combined assets under management (AUM) of the household. For our complete fee schedule, including a fee calculator for a potential portfolio, see the chart above.

Please review our Disclosure Documents for a comprehensive understanding of our services and fees.

Q: Is AIS active or passive?

We see “passive versus active” as a spectrum of possibilities as opposed to an “either/or” question. A strictly “passive” investor would buy every possible investment in the universe, which would result in more fixed income than stocks and a roughly equal split between U.S. and international stocks. Our typical portfolios, on the other hand, favor stocks over bonds for long-term growth, and are over-weighted toward U.S. stocks. Our “tilts” toward small cap and value move us further from a “passive” portfolio.

Despite these “active” tilts, we do not try to predict returns. We make no attempt to “time the market” or “pick” stocks. We tend to prefer investment vehicles that are relatively more “passive” in their approaches. Passive investment vehicles are able to provide broad market coverage at a lower cost than actively managed funds. However, the DFA funds we primarily use are not beholden to an index and have several trading advantages over strictly passive index funds.

We are responsive to changes in investor circumstances. We think of this as “situationally active.” When your life changes, we will analyze your holdings and alter your allocation plan if necessary.

The bottom line is that we are disciplined. We tend to hold investor portfolios unchanged for many years, and we would be considered “passive” as compared with many other investment advisors. This discipline has paid off historically as investors have avoided the urge to sell during markets downturns and potentially miss the subsequent recovery.

Q: Can I do it myself?

A: Potentially. Much of the value we add comes through the discipline to stay the course through the ups and downs of markets. Many investors may be able to maintain this discipline without our help.

In addition to discipline, we add value by: 1) offering DFA funds, which are generally only available through a select group of approved investment advisers; 2.) providing financial planning analysis to help develop a prudent portfolio structure; 3.) managing accounts in a tax-efficient manner; and 4.) providing comprehensive asset management across accounts to ease the burden of managing separate accounts.

Let our experience be your guide