In February 2010 the newly elected government of George Papandreou announced that Greece’s 2009 deficit was much larger than previously reported and revised it upward to an alarming 12.7 percent of GDP. This figure was more than double the previous government projection, and was later revised yet again, to 15.4 percent.

This turned out to be the tip of the iceberg of an escalating and unsustainable series of debt to GDP revisions and cascading drops in confidence in the sovereign debt of the peripheral Eurozone nations, particularly Portugal, Ireland, Greece and Spain the so called “PIGS” (sometimes expanded to include Italy).

Despite several rounds of rescue packages coordinated by the European Central Bank and International Monetary Fund from 2010 to 2012, world markets vacillated daily on the possibility that Greece would default on its sovereign debt and leave the Eurozone. It was feared this scenario (dubbed the “Grexit” by the financial press) would trigger a domino effect and that other highly indebted PIGS would quickly follow and put the viability of the Euro in question.

Credit spreads widened and the cost of insuring against default spiked for all of the peripheral countries, reflecting a lack of confidence in both the credit worthiness of the individual sovereign borrowers and the ability of the European authorities to contain the crisis.

Greece is a relatively small economy that represented less than twopercent of total 2011 European Union GDP. How could such a small nation cast such a large shadow over world markets? Perhaps investors recalled familiar claims in 2008 that the U.S. sub-prime market was insignificant in size and that the crisis would be contained, or that two failed Bear Stearns hedge funds would have no material impact on the bank’s solvency.

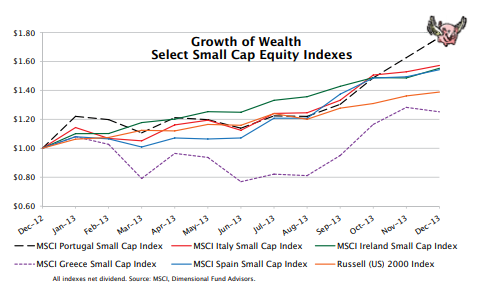

There was a very real risk of a Greek default that would spread to other nations, and world equity markets reflected that risk. But default did not ensue and investors ultimately were rewarded handsomely for assuming that risk. Portugal led the PIGS out of the crisis, where small cap stocks posted a 76.65 percent return for 2013. Ireland, Greece and Spain had very strong 2013 as well, as depicted in the accompanying chart.

Cassandras’ predictions of a European collapse never came to be. However this episode is instructive because it demonstrates how seemingly momentous developments in the world economy with horrific potential consequences are quickly digested and incorporated into capital market prices. Through this mechanism risky assets are clearly identifiable and distinguishable from safer investments. Investors are free to choose which assets to embrace, and which to avoid.

Also in This Issue:

Media Hype, the Informed Investor, and Free Markets

Future Testing

Active Managers versus Free Markets

The High-Yield Dow Investment Strategy

Recent Market Statistics

The Dow-Jones Industrials Ranked by Yield

Asset Class Investment Vehicles

To access the full article, please login or subscribe below.

Already a Subscriber?

Log in now

Subscribe Today

Get full access to the Investment Guide Monthly.

Print + Digital Subscription – $59/YearIncludes 12 Print and Digital Issues

Print + Digital Subscription – $108/2 Years

Includes 24 Print and Digital Issues

Digital Subscription – $49/Year

Includes 12 Issues

Digital Subscription – $98/2 Years

Includes 24 Issues