Our parent, AIER, recently reported on misapprehensions over the United States capital-account surplus and corresponding current-account deficit, which have persisted since 1982 (see Research Reports, No. 11, June 10, 2002). Critics assert that the current situation reflects foreigners paying for our profligacy, but they miss the point. The capital surplus is very large because the U.S. has been regarded for more than a decade as the best place in the world to invest. Our reasonably transparent capital markets and relatively unregulated economy are highly appealing and have fostered a continuous flow of investments from abroad.

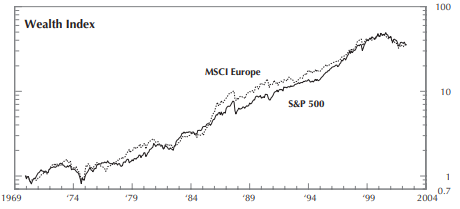

We will not speculate as to what might bring the current state of affairs to an end, but we cannot rule out a reversal in foreign investment here, so investors should have a stake in foreign assets. Indeed, the iShares Europe 350 Index fund and the MSCI EAFE Index, on which the Vanguard European Index fund is based, were up 4.82% and 7.75%, respectively, on a total return basis over the three months ending May 31. Meanwhile U.S. large-caps, the stellar performers of the 1990s, were down -0.74%. (See chart below for a long-term view.)

Many reasons are being cited supporting the notion that the current trend will persist. Wall Street produces an endless supply of “experts” ready to explain the trend du jour. Some have pointed to recent developments that might be rattling foreign confidence in U.S. markets, including meager interest rates, accounting chicanery among major corporations, and the expanded threat of terrorism. Even in the April 2002 Investment Guide, we pointed out that in historical terms U.S. stocks, relative to their underlying book value, were as highly valued as they have ever been. But we have no way to gauge whether we will witness substantial capital flight over the ensuing months. We continue to assert that current prices reflect the market’s estimate of tomorrow’s value, based on information available today.

If foreigner investors do reverse course, it is more likely that they would pare back their U.S. investments, rather than flee in panic. If so, most U.S. investors should continue to devote between 5-10% of their portfolios to the equities of developed foreign economies.

Also in This Issue:

Bankruptcy and the Safety of Pension Benefits

Life Insurance

Life Insurance Web Sites: Death of the Salesman?

The High-Yield Dow Investment Strategy

Recent Market Statistics

The Dow-Jones Industrials Ranked by Yield

To access the full article, please login or subscribe below.

Already a Subscriber?

Log in now

Subscribe Today

Get full access to the Investment Guide Monthly.

Print + Digital Subscription – $59/YearIncludes 12 Print and Digital Issues

Print + Digital Subscription – $108/2 Years

Includes 24 Print and Digital Issues

Digital Subscription – $49/Year

Includes 12 Issues

Digital Subscription – $98/2 Years

Includes 24 Issues