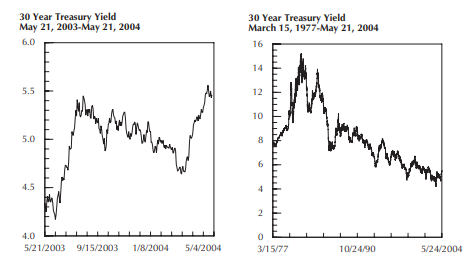

The month of April ushered in news signaling very solid economic growth, and the bond market responded by sending interest rates to their highest level in a year, as shown in the first chart below.

Conservative investors who have structured their portfolios in accordance with our recommendations might be anxious about the decline in their portfolio values, as bond prices have been pummeled in this environment. After all, we recommend that conservative investors have as much as 65 percent of their holdings in money market funds or fixed income investments. A shift in interest rates, however, is no reason to alter your investment strategy. We recommend only fixed income securities with maturities up to 5 years, which are far less interest rate sensitive than longer-term holdings. Moreover, while these interest rate spikes occur on occasion, cash and short-term bonds have proven to be far less volatile than equities over the longer term.

The fact is short-term interest rates simply cannot be forecast with any consistency. Rates are affected by a myriad of factors, not the least of which is the release of economic statistics. In April the market seized upon every bit of evidence that might have affected the Federal Reserve Board of Governors’ decision to alter the target fed funds rate; several reports regarding economic growth “exceeded the market’s expectations” and these were met by an immediate and sharp drop in bond prices. For months pundits have been warning that “rates have nowhere to go but up”, but when and by how much was anyone’s guess. It was new information that caused the latest spike; news by definition comes randomly, so security prices and interest rates move in a pattern that is inherently random.

Long-term interest rates remain below their long-term levels, as shown in the second chart below, but it does not follow that higher interest rates are imminent.The best estimate of tomorrow’s interest rates, in light of currently available information, is today’s rates. The best fixed income strategy to follow is one that ignores interest rate forecasts, either by holding a bond ladder or by following a variable maturity strategy (or “riding the yield curve”). Both were last described in detail in the March 2001 INVESTMENT GUIDE.

Also in This Issue:

Is an Adjustable Rate Mortgage for You?

Gold Revisited

The High-Yield Dow Investment Strategy

Recent Market Statistics

The Dow-Jones Industrials Ranked by Yield

To access the full article, please login or subscribe below.

Already a Subscriber?

Log in now

Subscribe Today

Get full access to the Investment Guide Monthly.

Print + Digital Subscription – $59/YearIncludes 12 Print and Digital Issues

Print + Digital Subscription – $108/2 Years

Includes 24 Print and Digital Issues

Digital Subscription – $49/Year

Includes 12 Issues

Digital Subscription – $98/2 Years

Includes 24 Issues