Occasionally, our Professional Asset Management clients ask us why they should continue to hold gold, which as an investment has been dismal since the early 1980s relative to other assets. Our response is that this has been a period of remarkable economic growth and modest price inflation, so gold has been neglected. However, we would no sooner sell gold in this environment than we would recommend canceling a health insurance policy simply because one has enjoyed a period of excellent health.

We continue to recommend gold related assets as an indispensable component of a well-structured portfolio. Many other passive-investment managers reject gold because strict adherence to “mean variance” analysis dictates that the gold price has been far too volatile relative to its long- term returns. We think this view is far too simplistic. The accompanying article by the World Gold Council corroborates our view that during periods of extreme stress, there is no substitute for gold and, furthermore, it indicates that holding gold is consistent with modern portfolio theory.

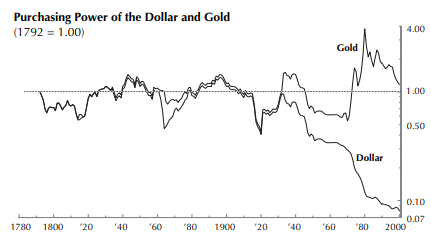

AIER’s long-time readers do not need mathematical models to be convinced. It was only during the 1970s that the financial world appeared to be collapsing. A severe recession was underway, and skyrocketing price inflation had prompted price controls. The Federal Reserve appeared rudderless and the executive branch had collapsed amid scandal. Communism appeared to be in ascension throughout the world. As these events unfolded, our predecessors were calling for investors to increase their gold holdings. Between 1968 and 1980 the gold price surged from $35.00 to $850.00 while the real value of most financial assets plummeted.

Our research tells us that altering a portfolio in anticipation of such developments (i.e. market timing) is inadvisable. Rather, investors should build “all weather” portfolios with adequate exposure to assets with desirable risk/return characteristics. Gold, in this view, is a form of insurance; unlike other asset classes, its value often becomes apparent only when it is needed.

Also in This Issue:

Managing Portfolio Risk For Periods of Stress: Gold’s Role in Efficient Portfolios

Will the Business Slowdown Become a Recession?

Newly Recommended Funds

The High-Yield Dow Investment Strategy

Recent Market Statistics

The Dow-Jones Industrials Ranked by Yield

To access the full article, please login or subscribe below.

Already a Subscriber?

Log in now

Subscribe Today

Get full access to the Investment Guide Monthly.

Print + Digital Subscription – $59/YearIncludes 12 Print and Digital Issues

Print + Digital Subscription – $108/2 Years

Includes 24 Print and Digital Issues

Digital Subscription – $49/Year

Includes 12 Issues

Digital Subscription – $98/2 Years

Includes 24 Issues